How To Develop Your Own Cryptocurrency Coin?

Tags: blockchain auditor • blockchain technology • crypto coin • cryptocurrency • digital currency • digital money

Everybody these days is aware of cryptocurrency or have tried their hand at investing in crypto coins like Bitcoin, Ethereum, or other popular Altcoins.

Did you know you could develop your own cryptocurrency like Bitcoin and Ethereum? Do you also know you can even give it a value and restrict the quantity of crypto coins you may generate?

But, before we get into how you can create your own digital coin, let us first learn more about crypto currency and how they are developed. Sounds good?

What is a cryptocurrency, and who created it?

Cryptocurrency functions similar to traditional currency in that it has a monetary value and can be easily exchanged and traded, with the exception that it is entirely digital and no one controls it.

Difference Between a Coin and a Token

A normal individual would not know the difference between a token or a coin. Only those who are familiar with cryptocurrencies and understand how it function would understand the distinction between a coin and a token.

Although both coins and tokens are cryptocurrencies, they are technically distinct. The first – Coin- has its own blockchain, such as Bitcoin, Litecoin, or Dogecoin, while the second – Token – lives on top of an existing blockchain framework such as Ethereum and NEO.

Blockchain technology is like an operating system such as Windows or MacOS on top of which cryptocurrencies run as a software.

Examples of tokens are Tether (USDT), Shiba Inu, BAT (Basic Attention Token), Dogecoin, UniSwap, and there are hundreds more.

Ethereum is a very popular blockchain, it’s coin is called Ether and it’s token is called ERC20 tokens.

In a nutshell, a coin is a digital currency with monetary value that can be used to purchase merchandises and services and even tokens, whereas a token is an asset or deed, as in smart contracts but it cannot buy a crypto coin.

When a coin is spent, it does not move from sender to receiver; rather, their respective accounts are simply updated, similar to bank transactions. Whereas a token physically moves, as in NFTs (non-fungible tokens) where the ownership of the token is manually updated. Just like cash where the money changes hands and moves physically.

What is Crypto Mining and Minting?

Mining cryptocurrency is a process in which miners or users employ sophisticated hardware resources to verify and record each transaction in the blockchain ledger in exchange for a coin they receive as a reward.

Cryptocoin Miners must solve exceedingly complicated mathematical problems as part of the mining process in order to get rewards. The first miner to solve the computational challenge earns a coin; other miners in the system are assigned other problem to solve in order to receive another coin as a reward.

Each awarded coin is introduced to the system for trade and circulation.

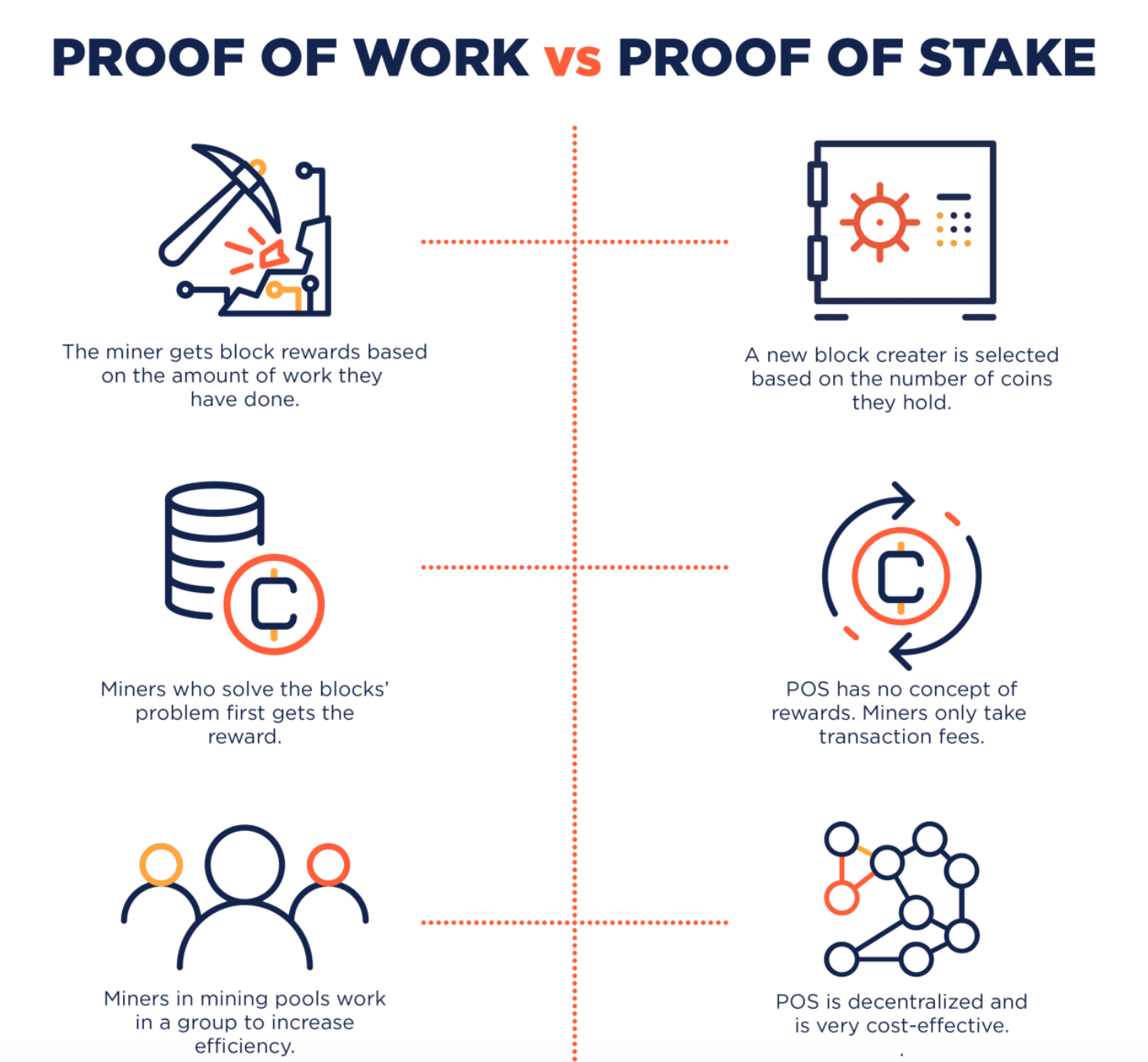

Minting Crypto on the other hand is a process in which new coins are generated through authenticating data, creating new blocks, and recording the information onto the blockchain through a “proof of stake” (PoS) mechanism.

Proof of stake (PoS) is a cryptocurrency protocol where coin owners offer crypto coins they own as collateral for getting a chance to process and authenticate transactions and create new blocks in a blockchain. Thus proof-of-stake involves a network of Coin owners or “validators” who “stake” — their coins in exchange for a chance to validate a new transaction and get a reward in return. The more coins a validator has for stakes, the more likely it is that he or she will be chosen to validate a new transaction.

Another consensus mechanism used to verify transactions is “proof of Work” (PoW). Proof of work utilises crypto mining to achieve transaction verifications and adding a new block in the blockchain.

Of the two consensus mechanism mentioned above to verify crypto transactions, Proof of work is the older of the two, used by Bitcoin, Ethereum 1.0, and many others. Proof of stake, on the other hand is the newer technology and it is used by Ethereum 2.0, Cardano, Tezos and other newer cryptocurrencies.

We are confident that you now understand what a cryptocurrency is and how it functions. Let’s get right to how we can create one for your company or brand.

Below are the steps through which you can develop your own cryptocurrency:

Step 1 – Decide The Objective & Goal For Your Crypto Coin

Before you begin developing your own digital coin, consider what the crypto coin’s goal is and what benefits it will provide for your organisation. Answer some of these questions to arrive at a strategic decision to have your own cryptocurrency or not.

Do you plan to accept crypto currency for your product or services? Do you believe the transaction in crypto coins will benefit and boost your business?

Step 2 – Decide Which Consensus Mechanism To Deploy

Because blockchain technology is a decentralised system, the validity and legitimacy of a transaction can only be determined and recorded through consensus mechanisms (protocols). The most commonly used consensus mechanisms are proof of work (PoW) and proof of stake (PoS) explained above.

The Nodes in your blockchain system will use the chosen consensus mechanism to verify every transaction.

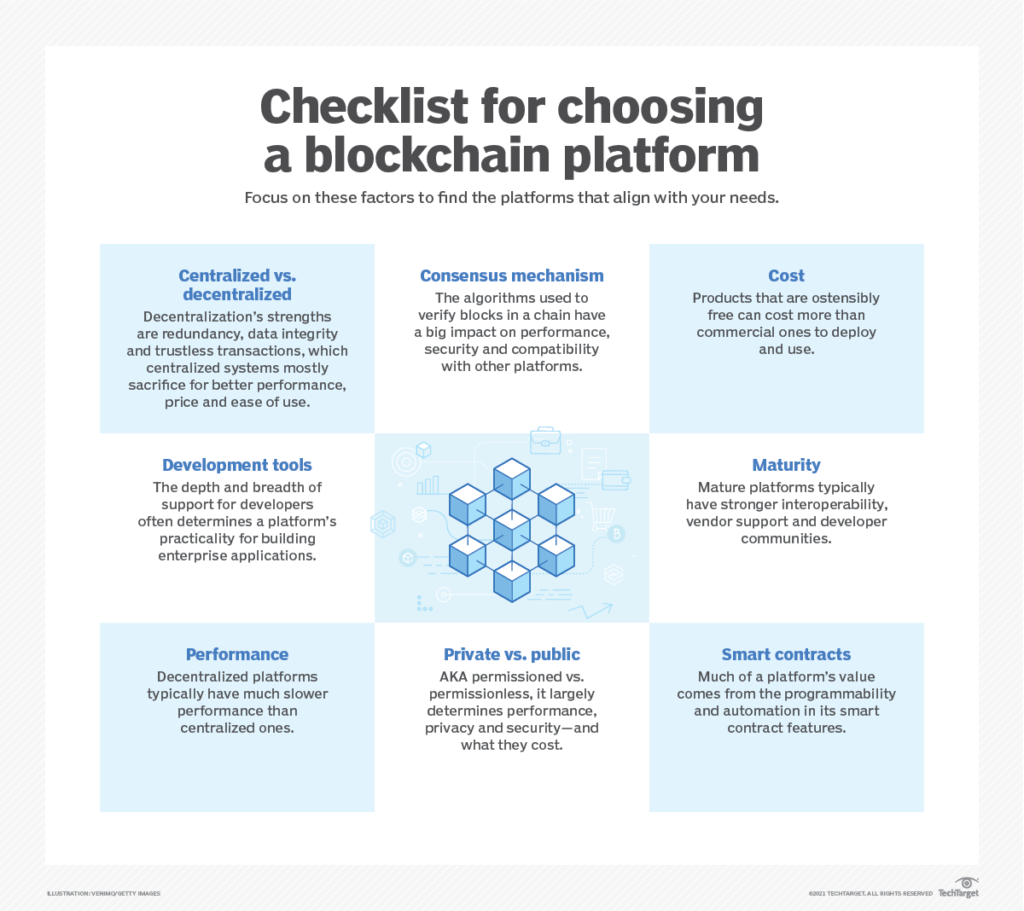

Step 3 – Decide On The Right Blockchain Technology To Adopt

The right blockchain technology will depend on your choice of consensus mechanism you select in the previous step.

Blockchain technology platforms are made up of a number of components, allowing blockchain developers and enterprises to select the optimal combination of components to achieve a certain goal.

When selecting a blockchain platform, numerous factors must be considered, including performance, energy usage, and the cost.

Some of the popular blockchain architecture are as follow:

- Ethereum (oldest and most established blockchain platform; comparable to Bitcoin blockchain)

- IBM blockchain (private and decentralized blockchain network)

- Hyperledger Fabric (hosted by Linux Foundation, developed especially for enterprise distributed ledger)

- Stellar (relatively new platform optimized for DeFi (Decentralized Finance) applications)

Step 4 – Design The Nodes & Blockchain Internal Architecture

To put it simply, nodes are internet-connected computers/devices that serve the blockchain system by performing specialised tasks such as validating and processing transactions and finally storing the block data using the consensus method.

You now understand who employs the true consensus mechanism to validate each blockchain transaction. When a user joins a blockchain network, they effectively become nodes of the network.

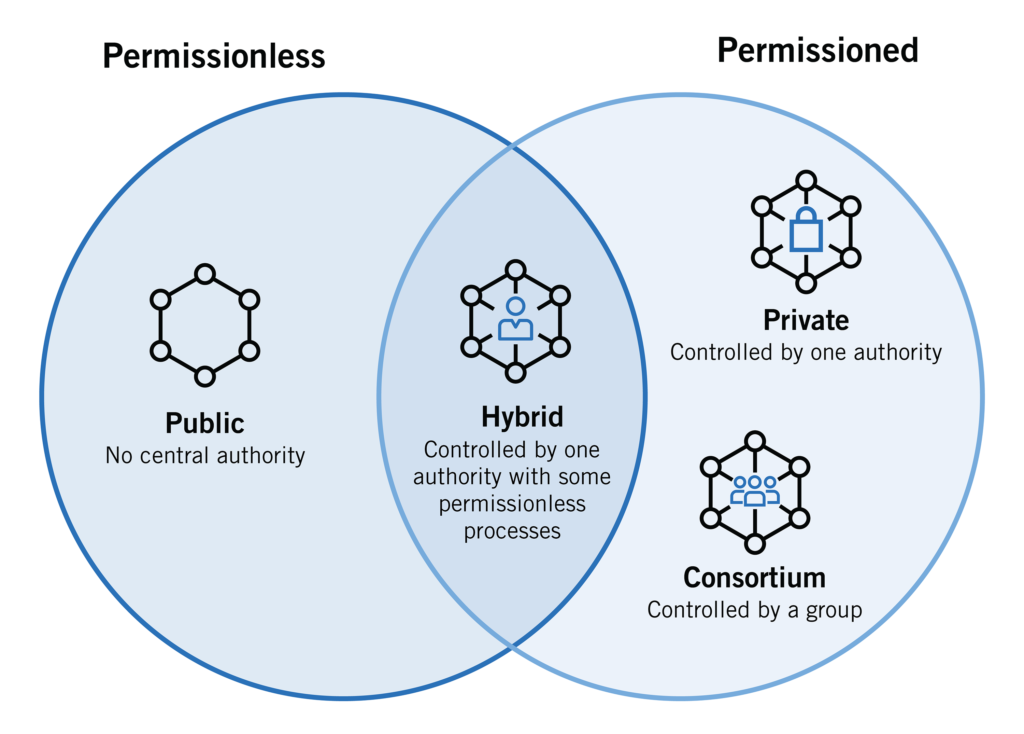

The sort of blockchain architecture you choose determines whether these nodes have permission, do not have permission, or a combination of both to be part of your blockchain network.

The permissionless blockchain design allows any user or node to join the blockchain network. A permissioned blockchain network, on the other hand, only enables specified nodes to join the network.

Each blockchain architecture has advantages and disadvantages. For example, permissionless blockchain networks are more secure than permissioned blockchain networks since there are many nodes that collaborate to validate each transaction block. In a permissioned blockchain, only approved nodes may verify transactions, and specific nodes may collude while validating transactions.

Permissioned blockchains are more efficient than permissionless blockchains since there are fewer nodes to verify transactions, resulting in less energy spent by these resources during consensus mechanism.

After selecting whether your blockchain network will be permissionless, permissioned, or both, the next step is to select a blockchain architecture.

Following are the type of blockchain architecture:

- Public – permissionless and decentralized blockchains

- Private/Managed – permissioned and centralized blockchains

- Consortium – permissioned blockchains

- Hybrid – centralized with little permissionless properties

Once the blockchain design has been finalised, the blockchain code must be audited to remove any vulnerabilities. Hire expert blockchain auditors to examine the code since changing particular parameters would be tough after the coin is produced and the blockchain is operational.

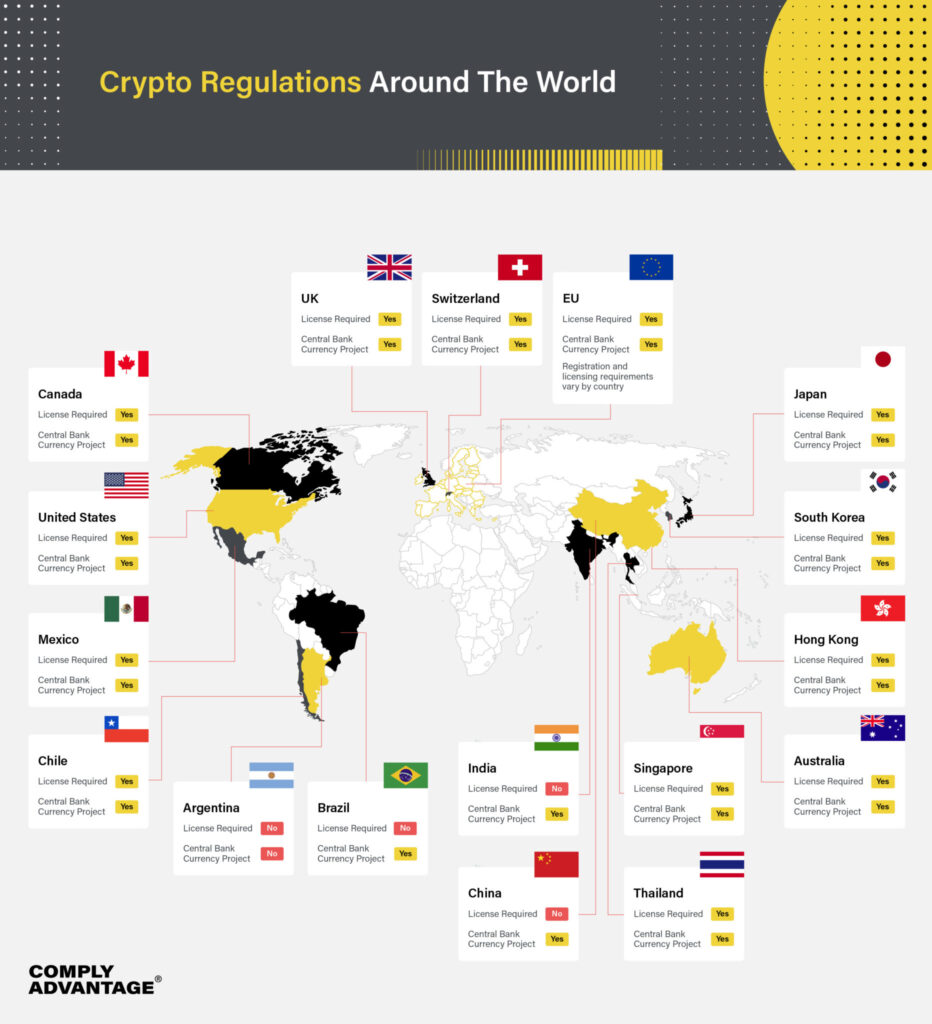

Step 5 – Comply With The Legal Laws & Regulations

It is critical that the crypto coin generated adheres to legal rules and regulations, lest it be outlawed in countries where it does not. So, it is recommended to hire a legal expert who deals in cryptocurrencies and understand the laws and regulations.

What this means is that the cryptocurrency developed should confirm with the regulations from the Securities and Exchange Commissions (SEC), the Federal Trade Commissions and Commodities Trade Commissions of respective countries.

As a blockchain development company, we understand the significance of such rules and regulations and can assist you in complying with local legislation at the development level.

Forking an existing blockchain is another alternative if you want to produce cryptocurrency without coding or have a low budget. Forking is the process of modifying an existing blockchain source code in order to create your own digital coin.

Because blockchain technology is open source, you can readily obtain the source code from the GitHub site.

Previous Post

Previous Post Next Post

Next Post